INCLUSIVE FRAMEWORK ON BEPS

OECD (2024), Pillar One – Amount B: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris.

Background

The OECD released a final report on Amount B in February 2024, with updates finalized in June 2024. This report provides a framework for determining arm’s length prices for specific marketing and distribution activities. Countries can choose to implement this simplified approach, known as Amount B, to enhance tax certainty and reduce disputes for resident distributors.

Amount B offers a simplified approach to transfer pricing for basic marketing and distribution activities. It uses a standardized framework with predetermined remuneration levels for low-risk distributors. This aims to streamline the process, reduce disputes, and promote a more consistent application of the arm’s length principle. By making transfer pricing easier and more transparent, Amount B’s goal is to benefit both taxpayers and tax authorities, particularly in less developed countries. Its overall impact will depend on how widely (and consistently) is adopted globally.

While countries have the autonomy to choose if, and how, they implement Amount B, its application is globally standardized to tax years beginning on (or after) January 1, 2025.

Scope of application

Unlike Amount A, Amount B is not limited to only large groups. The regulatory framework applies to multinationals using intra-group low-risk distributors for sale of goods to independent companies.

Amount B applies to all multinational businesses using low-risk distributors to sell goods to independent companies, regardless of the scale. This means, any company utilizing this type of distribution structure could potentially be affected by Amount B.

Nevertheless, to conclude on Amount B’s applicability, some factors need to be verified:

- Firstly, the Transactional Net Margin Method (TNMM) is selected as best method[1] to analyze the transaction with the distributor being the tested party.

- Quantitative criteria must be met, specifically, the distributor cannot have a ratio of OPEX/Sales under 3%, or above the 20 to 30% range (with the value being determined by the country).

- Focus on wholesale distribution activities (small volumes of consumer sales, i.e., under 20% are accepted) as well as the activities of sales agents and commissioners. In short, any functions beyond those of baseline marketing and distribution activities would be covered by this initiative.

- All types of consumer and industrial products are included; however, intangible goods, commodities or services are not.

Remuneration defined in Amount B

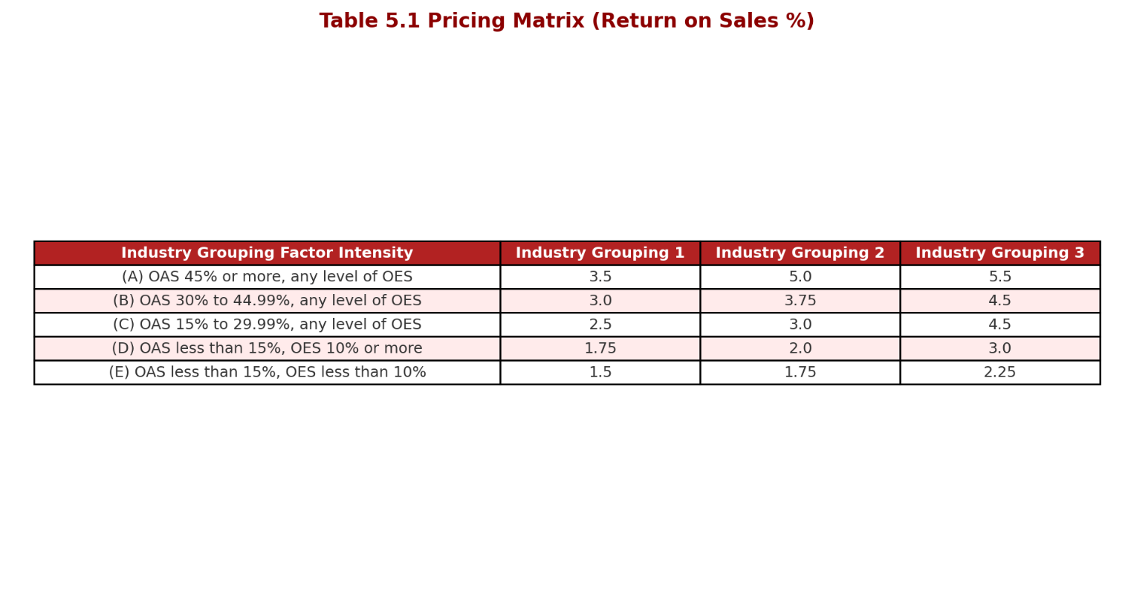

The company’s compensation is done using a predefined price matrix allowing for a target return on sales (ROS) for the tested party based on its characteristics.

The matrix recognizes different parameters, these reflect i) industry grouping, as well as ii) differentiated levels of factor intensity (based on their operating assets and expenses relative to their sales).[2] Multiple scenarios are identified, each with a predefined profit margin ranging from 1.5% to 5.5%, allowing for a fixed range of +/- 0.5% around the standardized margin instead of an interquartile range.

The matrix (Table 5.1[3]) is shown as follows:

Going into further detail, the guideline defines three steps for its application to in-scope transactions:

- Step 1: Select the industry grouping (1[4], 2[5] or 3[6]) and identify the applicable column.[7]

- Step 2: Determine the factor intensity classification[8] (i.e., A, B, C, D and E) and identify the applicable row.

- Step 3: Identify the range corresponding to the intersection of the above parameters.[9] This will result in a range based on the +/- 0.5% interval around the corresponding return on sales as per the matrix. Any point within that acceptable range can be relied upon.

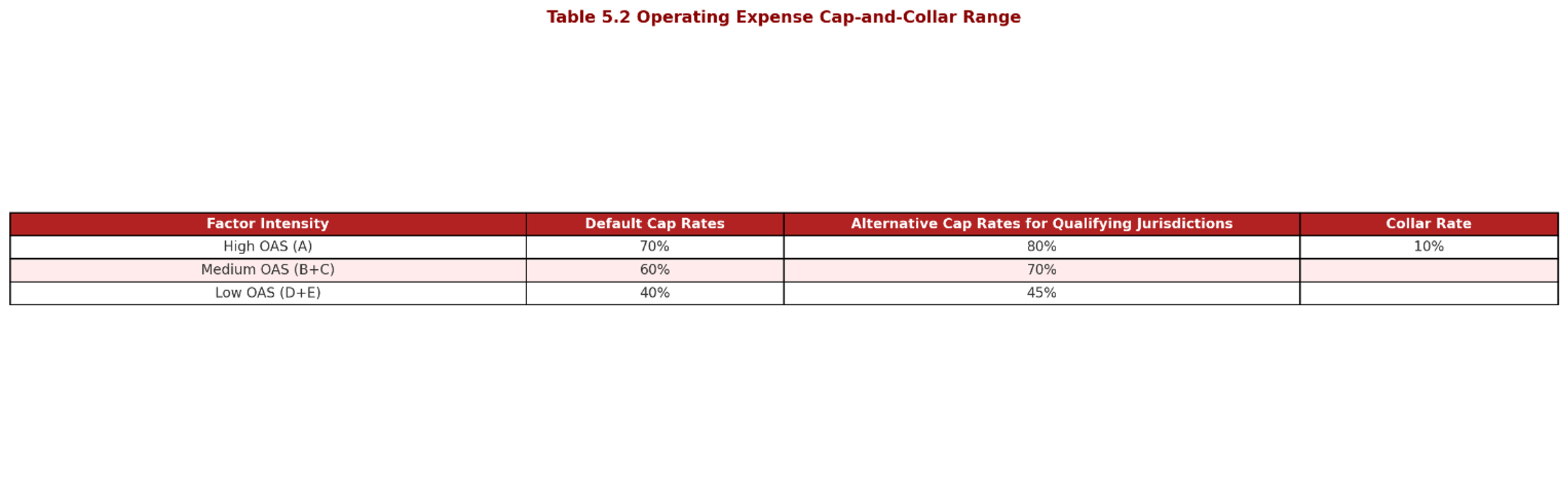

The document includes additional procedures to ensure arm’s length outcomes, once Step 3 (above) is completed. These are a) Operating expense cross-check, and b) Data availability mechanism for qualifying jurisdictions.[10]

The application of the operating expense cross-check allows the tested party’s profitability to be adjusted when the return on sales profit indicator produces a result outside of the pre-defined operating expense cap-and-collar range as specified in table 5.2[11] of the document,[12] otherwise no adjustment is warranted.

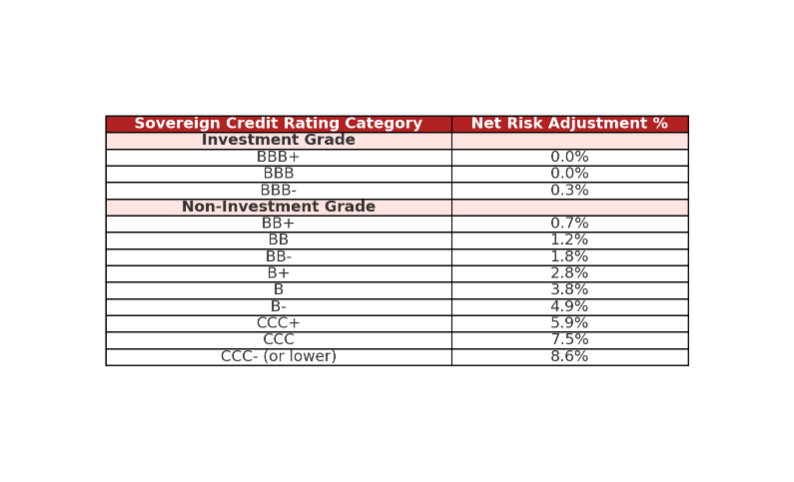

The second additional procedure refers to the data availability mechanism (for qualifying jurisdictions). Essentially, it aims to implement an adjustment for tested parties within certain qualifying jurisdictions, focused on those countries that may be under-represented or outright excluded from the global datasets employed to derive the ROS targets (which will be periodically adjusted). This adjustment is defined by reference to the sovereign credit rating of the qualifying jurisdiction. It should be noted that a “qualifying jurisdiction” is likely a country identified as having a higher risk profile, often based on factors like sovereign credit ratings. These jurisdictions might face challenges in attracting investment or have less developed economies.

Where a tested party is located in a qualifying jurisdiction, an adjustment will be made to the ROS. The tested party in a qualifying jurisdiction will earn an adjusted return as per this formula[13]:

Adjusted return on sales = ROS + (NRA x OAS)

Where:

ROS is the return on sales percentage of the tested party.

NRA is the net risk adjustment percentage of the qualifying jurisdiction derived from table below, and,

OAS is the net operating asset intensity percentage of the tested party for the relevant fiscal year (it will not exceed 85% for the purpose of computing this adjustment).

Any point in the adjusted range (or the base range if no adjustments are necessary) can be relied upon for compliance purposes for in-scope transactions.

Limitations and current state of play

Conceptually, Amount B should simplify transfer pricing compliance by providing a streamlined approach. However, as it is an optional initiative, it is too early to conclude on its effectiveness. Moreover, since countries choose whether to adopt Amount B (and, how to implement it), inconsistencies are likely to arise. In fact, in September 2024, the OECD published a Model Competent Authority Agreement to (preemptively) assist countries in resolving potential double taxation issues related to Amount B.

As of the end of 2024, the European Union is progressing with its directive to implement Pillar One, including Amount B, within its member states, although there is no clear timeline for finalization. While many countries have expressed interest in Amount B, formal progress towards its application remains uneven. This situation requires close monitoring, especially as Amount B can be applied from January 1, 2025 onwards.

To illustrate potential inconsistencies, consider the Dutch approach. A December 4, 2024 decree states that the Netherlands will not apply Amount B domestically (to local distributors) but will accept its application in “covered jurisdictions” listed by the OECD. This means the Netherlands will adjust transfer prices to prevent double taxation if a covered jurisdiction incorporates Amount B into its regulations, applies it correctly, and has a tax treaty with the Netherlands. Another likely inconsistency is in the US, where the new Trump administration is unlikely to be a strong champion for any BEPS initiatives, including Amount B.

The lack of uniformity in implementation has created uncertainty and may lead to potential disputes, especially in cross-border transactions across jurisdictions with varying Amount B approaches as, in practice, unless fully implemented by all parties involved, traditional transfer pricing rules will coexist with Amount B postulates. This inconsistency will inevitably lead to greater complexity and a dilution of the potential benefits of Amount B. Furthermore, the pricing matrix itself may prove more complicated in practice than anticipated, despite being designed to simplify profit allocation.

It is crucial for multinational entities to proactively assess and monitor Amount B developments. BaseFirma is assisting our clients in evaluating risks and opportunities related to prospective Pillar One implementation, including an assessment of current transfer pricing policies compared to Amount B-compliant policies.

Please reach out to us for additional information at paul.valdivieso@basefirma.com

[1] Amount B should not be applied where the CUP method, using internal comparables, can be reliably applied and the necessary information is readily available to tax administrations and taxpayers.

[2] OES refers to ratio of operating expenses to net revenue, and OAS refers to ratio of operating assets to net revenue.

[3] OECD (2024), Pillar One – Amount B: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris. Table 5.1.

[4] Perishable foods, grocery, household consumables, construction materials and supplies, plumbing supplies and metal.

[5] IT hardware and components, electrical components and consumables, animal feeds, agricultural supplies, alcohol and tobacco, pet foods, clothing footwear and other apparel, plastics and chemicals, lubricants, dyes, pharmaceuticals, cosmetics, health and wellbeing products, home appliances, consumer electronics, furniture, home and office supplies, printed matter, paper and packaging, jewelry, textiles hides and furs, new and used domestic vehicles, vehicle parts and supplies, mixed products and products and components not listed in group 1 or 3.

[6] Medical machinery, industrial machinery including industrial and agricultural vehicles, industrial tools, industrial components miscellaneous supplies.

[7] In the case that the products distributed fall into more than one industry grouping, the proportion of sales falling into each industry grouping should be calculated. In the case that at least 80% of sales fall into a single industry grouping and so 20% of sales or less fall into different industry grouping(s), the latter will not be determinative for setting the matrix return and instead the return will be set by reference only to the relevant matrix cell for the industry grouping where the majority of sales fall. In the case that more than 20% of sales are from products which fall into a second and/or third industry grouping, a weighted average return should be calculated.

[8] The factor intensity classification of the tested party should be calculated based on a weighted average of the three preceding fiscal years.

[9] If needed, the weighted average return should be calculated by multiplying each return from the relevant cells of the matrix by the proportion of sales to be priced by reference to that cell and totaling these proportional returns to give a single weighted average return rate applicable to all sales by that distributor.

[10] Refers to low or middle-income countries, often with limited data availability or specific economic conditions. The current OECD list includes over 100 countries, although it should be noted that this does not imply that these jurisdictions are obligated to adopt (or will adopt) the amount B approach.

[11] OECD (2024), Pillar One – Amount B: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris. Table 5.2.

[12] Essentially comparing the Equivalent Return on Operating Expense (EROE) of the tested party against the operating expense cap-and-collar. If the Equivalent Return on Operating Expense (EROE) of the tested party exceeds the operating expense cap, the return on sales of the tested party will be adjusted downwards until it results in an equivalent return on operating expense equal to the operating expense cap. Conversely, where the equivalent return on operating expense of the tested party falls below the operating expense collar, the return on sales of the tested party will be adjusted upwards until it results in an equivalent return on operating expense equal to the operating expense collar. The EROE is equal to the ROS divided by the Operating Expense Percentage (i.e., OpEx/Sales).

[13] OECD (2024), Pillar One – Amount B: Inclusive Framework on BEPS, OECD/G20 Base Erosion and Profit Shifting Project, OECD Publishing, Paris. Table 5.3.